Refinancing used to sound simple. Interest rates dropped, you refinanced, and you saved money. End of story.

Today, the conversation is more complicated. Rates fluctuate. Economic headlines are noisy. Many people assume refinancing is no longer worth considering—especially if rates are higher than they were a few years ago.

That assumption may be costing you money.

Refinancing is not only about chasing the lowest interest rate. It is about strategy, structure, and long-term financial efficiency. In many situations, you might still want to refinance—even when conditions seem less than perfect.

This article explains why refinancing can still make sense, who should consider it, and how smart decision-makers evaluate refinancing beyond the headline rate.

What Refinancing Really Means

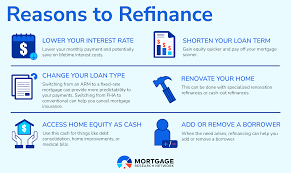

At its core, refinancing means replacing an existing loan with a new one under different terms.

Those changes may involve:

- A different interest rate

- A new loan term

- Lower monthly payments

- A change in loan type

- Improved cash flow or flexibility

Refinancing is not a single goal. It is a tool—and tools work best when used intentionally.

Why Many People Dismiss Refinancing Too Quickly

The most common mistake people make is focusing on one number: the interest rate.

If the new rate is not lower than the old one, many assume refinancing is pointless. That mindset ignores several important realities:

- Financial goals change

- Cash flow needs evolve

- Risk tolerance shifts over time

- Debt structure matters as much as cost

A higher rate does not automatically mean a worse outcome.

When Refinancing Can Still Be a Smart Move

There are several scenarios where refinancing may make sense—even if rates are not at historic lows.

1. To Improve Monthly Cash Flow

Lowering monthly payments can free up cash for:

- Emergency savings

- Debt reduction

- Investments

- Business opportunities

Extending the loan term or restructuring payments may increase total interest over time, but it can significantly improve short-term stability and flexibility.

For many professionals, cash flow matters more than theoretical long-term savings.

2. To Consolidate High-Interest Debt

Refinancing can be a powerful way to simplify finances.

Rolling multiple high-interest debts into a single, structured loan may:

- Reduce overall interest costs

- Lower stress

- Improve budgeting clarity

The key is discipline. Consolidation works only if new debt does not replace old habits.

3. To Switch Loan Types

Some borrowers refinance to change the nature of their loan, not just the rate.

Examples include:

- Adjustable-rate to fixed-rate

- Short-term to long-term stability

- Variable payments to predictable ones

This shift can reduce risk and uncertainty—especially during volatile economic periods.

4. To Remove or Add a Co-Borrower

Life changes. Relationships change. Financial responsibilities shift.

Refinancing can:

- Remove a former partner

- Add a spouse

- Simplify shared obligations

In these cases, refinancing is about control, not savings.

5. To Access Equity Strategically

In some situations, refinancing allows access to built-up equity.

Used carefully, this can support:

- Home improvements

- Business investment

- Strategic debt restructuring

Used carelessly, it increases long-term risk. Intention matters.

Why Executives and High-Income Earners Refinance Differently

For professionals and executives, refinancing is often less about survival and more about optimization.

High-income borrowers typically focus on:

- Liquidity management

- Tax efficiency

- Opportunity cost

- Balance sheet strategy

A refinance that slightly increases interest but improves cash flow or flexibility may still be a net win.

The Hidden Costs of Not Refinancing

Doing nothing is also a decision—and sometimes an expensive one.

Staying with the wrong loan structure can mean:

- Higher stress

- Reduced flexibility

- Missed opportunities

- Inefficient use of capital

The cost of inertia is often invisible, but real.

How to Evaluate Whether You Should Refinance

Instead of asking “Is the rate lower?”, ask better questions:

- What problem am I trying to solve?

- How long do I plan to keep this loan?

- How does this affect cash flow?

- What is the total cost over time?

- Does this improve or reduce flexibility?

Refinancing is a strategic decision—not a reflex.

Common Refinancing Mistakes to Avoid

- Chasing the lowest rate without considering fees

- Restarting long loans repeatedly without a plan

- Ignoring break-even timelines

- Using refinancing to fund lifestyle inflation

- Failing to adjust spending after refinancing

Refinancing should support discipline, not replace it.

The CEO Mindset: Debt as a Managed Tool

Strong leaders do not fear debt—but they manage it deliberately.

They understand that:

- The structure of debt matters

- Flexibility has value

- Cash flow is strategic

- Risk must be controlled

Refinancing is one way to realign debt with reality.

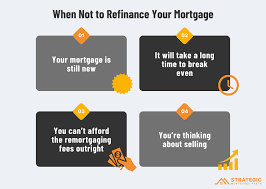

When Refinancing Is Probably Not a Good Idea

Refinancing may not make sense if:

- You plan to sell soon

- Fees outweigh long-term benefits

- The new loan increases risk unnecessarily

- The decision is driven by short-term emotion

Clarity should always come before action.

Final Thoughts: Refinancing Is About Fit, Not Headlines

You might still want to refinance—not because rates are perfect, but because your situation has changed.

The best financial decisions are rarely about timing the market. They are about aligning tools with goals.

Refinancing, when done thoughtfully, is not a sign of financial trouble. It is a sign of financial awareness.

Review your options. Run the numbers honestly. And make sure your debt structure works for you—not against you.

End of article.

Summary:

Even though rates are on the rise, that doesn’t mean you shouldn’t refinance.

Keywords:

refinance,finance

Article Body:

Even though rates are on the rise, that doesn’t mean you shouldn’t refinance.

Practically everyone has refinanced or thought about it at one point in time. We’ve seen the dozens of commercials that urge us to do it. With rates at record lows over the past few years, refinancing has helped many borrowers lower their monthly payments.

But rates are now on the rise. Refinancing applications have fallen slightly. Most people don’t think you should refinance when rates are going up. However, many refinancings are “cash-out” refinancing. That means that equity is handed over to the homeowner in return for a larger mortgage. Many people need that cash.

Some people are refinancing their homes for a “cash-out” because they have a significant home-equity line of credit balance. This line of credit has an adjustable-interest rate, which is going up on them. They refinance it in with their first mortgage at a fixed rate. They aren’t eliminating the debt, just fixing the interest rate and monthly payment. If you don’t need the revolving line of credit, you should probably take advantage of the fixed rate.

There are many homeowners that piggyback their mortgages when they are buying. They end up with one mortgage for 80% of the value of the home and a second mortgage for 10%. They put the remaining 10% down on the home. Since the first mortgage is only for 80% of the purchase price, they avoid having to pay PMI.

Many piggybackers have a line of credit as the second loan. Others simply want to consolidate into one loan that would be easier to keep track of. Either way, refinancing into a fixed-rate isn’t a bad idea. And one payment is easier to make on time each month than two.

Those out there with adjustable-rate mortgages are starting to get a little nervous. Interest rates have been rising pretty fast. The gap between the rate of a adjustable mortgage and a fixed mortgage has narrowed so much that you really don’t save much by taking the adjustable mortgage. Many are looking to avoid rising interest rates by financing to fixed-rate mortgages.

Refinancing can be a good thing. You can get a fixed rate to counter the rising interest rates. You can use cash from a refinancing to consolidate your debt. You can improve your home. But you should be careful about taking too much equity out of your home.

Many advisors warn consumers not to use their homes as personal piggy banks. If home prices decline, you could owe more than your house would sell for. In a cooling, or slowing, real estate market, you do not want to be maxed out on the equity in your home. If something happened and you had to sell, you want to walk away from the closing table with money, not have to go to it with a check. Paying to sell your home isn’t how you want to do it.

Fixed-rate mortgages are always a good and solid financial choice. Anytime you are looking to refinance, your best option is to go with the shortest-term, fixed-rate mortgage you can afford.

Tinggalkan Balasan